Menards: How a Self-Funded Lumberyard Took on Home Depot

Menards ranks No. 36 on NRF's Top 100 Retailers 2026. Here's how John Menard built a debt-free, self-manufacturing chain that outlasted its rivals.

Part of Retailer Playbooks — history-first profiles of every company on the NRF Top 100 Retailers list.

Menards lands at No. 36 on the National Retail Federation's Top 100 Retailers 2026 list, with $14.10 billion in 2025 U.S. retail sales, compiled with Kantar. It got there without a single outside investor, a public stock ticker, or, by most accounts, much patience for anyone who didn't clock in on time.

A Pole Barn Business That Outgrew Itself

John Menard Jr. grew up the oldest of eight kids on a Wisconsin farm run by teacher-parents, and he paid his way through Wisconsin State College at Eau Claire building post-frame pole barns, starting around 1958, two decades before Home Depot existed, according to Forbes. He graduated in 1962 or 1963 and, as the story goes, turned down a job offer from IBM to keep building.

The construction side led him into buying lumber in bulk and reselling it to other builders on weekends, when the regular lumberyards were closed. That side hustle grew faster than the barns did. By the time building supplies had eclipsed the construction business, Menard sold off the construction division and formally incorporated Menard, Inc. in 1972, according to FundingUniverse, just as the do-it-yourself remodeling boom was taking off across the Midwest.

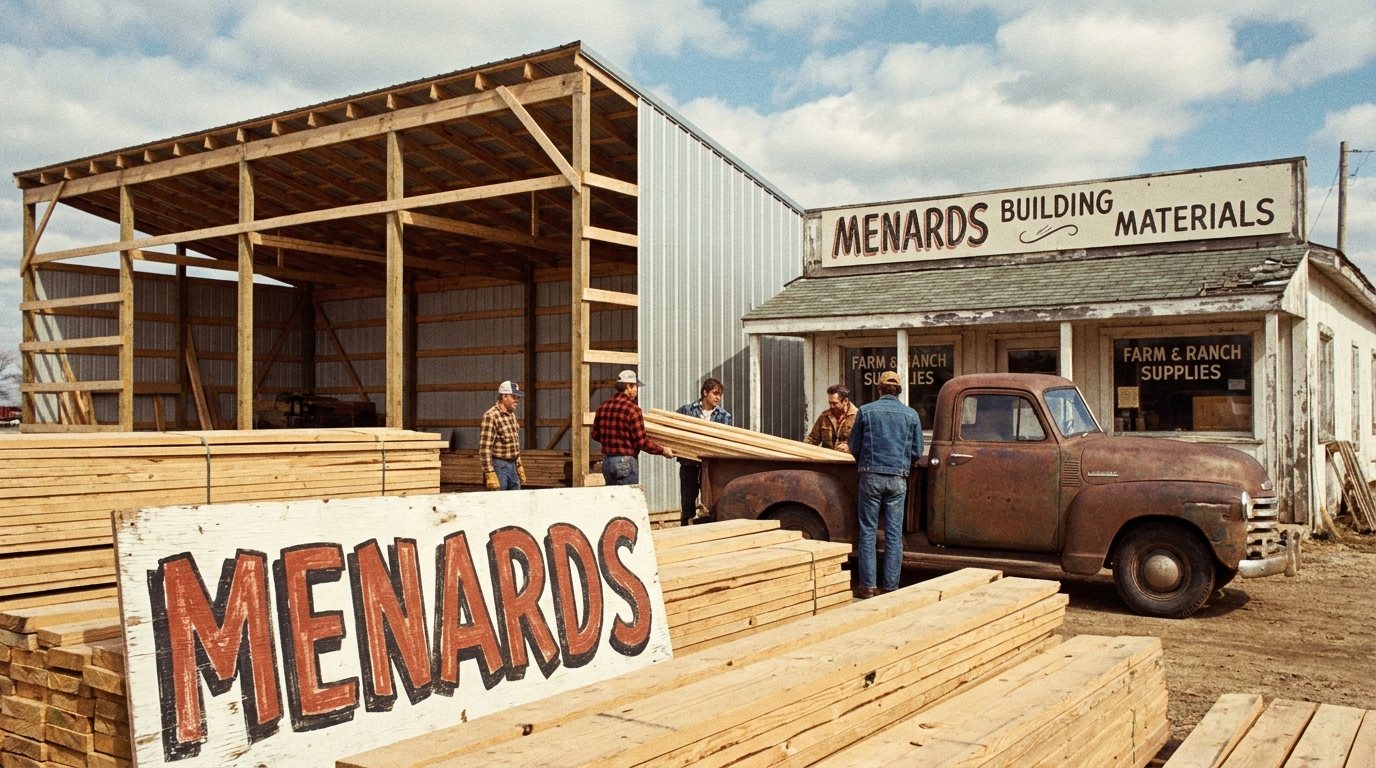

Building a Store That Didn't Look Like a Lumberyard

Menard's first real innovation wasn't pricing. It was format. Instead of copying the dim, cluttered lumberyard layout that defined the category, he built stores with wide aisles, tile floors, and shelving a regular customer could actually reach, closer to a mass merchant than a contractor supply house. He also bought cheap, well-located vacant retail real estate and filled shelves with a mix of seconds, overstock, and closeouts, a habit that kept margins workable even while prices stayed low.

The formula scaled through the 1970s and 1980s across Wisconsin, Iowa, Minnesota, and the Dakotas. By 1986, Menards was the 15th-largest home improvement chain in the country, with 34 stores and roughly $500 million in sales. Expansion picked up through the early 1990s into Nebraska, Chicago, Indiana, and Michigan, and by 1995 the chain had grown to 115 stores and $2.7 billion in sales, per FundingUniverse.

The Home Depot Test

Every regional hardware chain of that era eventually had to answer the same question: what happens when Home Depot shows up. For Menards, the answer arrived in September 1994, when Home Depot entered Chicago, a market Menards had only broken into in 1991. Trade press was skeptical. Forbes writer Frank Wolfe warned Menard would need to do "a lot better" to survive.

He did better by not blinking. Menards kept opening stores in the same market it was supposedly about to lose, and it was Menards' aggressive Chicago expansion, not Home Depot's, that is credited with helping push regional rival Handy Andy out of business. By 1998, Menards was running 139 stores and $4 billion in revenue. Lowe's arrived in Chicago at the turn of the century too; Menards held its ground there as well.

The lesson retail historians draw from this period isn't that Menards out-marketed Home Depot. It's that it refused to change its store economics under pressure, betting that a devoted regional customer base and a lower cost structure would outlast a national competitor's initial land grab. It did.

Owning the Factory Behind the Store

Here is the part of the Menards story that rarely makes it past the trade press: for decades, the company has manufactured roughly a quarter of what it sells. Steel doors, Formica countertops, picnic tables, even doghouses have come out of Menards-owned plants rather than a supplier's, a practice FundingUniverse pegs at saving the company something like 10 percent versus buying finished goods on the open market. Pair that with the highest sales-per-employee ratio among its major competitors, and Menards built a structural cost advantage that a purely retail-focused rival could not simply match by cutting a purchase order.

The Discipline Behind the Balance Sheet

The detail that best explains how Menards has stayed private, debt-averse, and expanding for more than fifty years without an IPO or a private-equity recap is not a strategy slide. It's the time clock. Forbes reports that Menard requires even top executives to punch in every morning, the same as any hourly associate. That's not a quirky anecdote. It's the operating culture that let a founder finance growth almost entirely out of store cash flow rather than borrowed capital or outside investors, a rarity among retailers of Menards' scale.

Vendors have described Menard over the years as tenacious to the point of frightening, and the company has drawn its share of lawsuits from employees, customers, and suppliers along the way, along with regulatory fines, including a $1.7 million hazardous-waste penalty in 1997. None of it slowed the expansion. Menard, unlike most retailers this size, never had to explain a quarter to shareholders, because there weren't any.

Where It Stands Now

Menards today runs more than 340 stores across 15 Midwestern and Mid-Atlantic states out of its Eau Claire, Wisconsin headquarters, still fully owned by John Menard Jr., now worth an estimated $17 billion according to Forbes' 2026 figures. It remains the third-largest home improvement retailer in the country behind Home Depot and Lowe's, a position it has now held for three decades without ever being acquired, going public, or taking on outside capital.

The through-line from the pole barns to the No. 36 ranking on the NRF list is consistency of ownership. A company that manufactures its own doorknobs and makes its regional presidents punch a clock is a company built to compound quietly, on its own terms, for a very long time.

Every retailer on this list runs on the same unglamorous infrastructure: what's on the shelf, what it costs to put there, and how well anyone can find it. Menards just happens to build more of that infrastructure itself than most.